Virtual Card for Expats: How to Pay Abroad

Moving abroad almost always starts with a financial challenge. You need to pay for temporary housing, leave a rental deposit, buy a local SIM card, connect internet, arrange insurance, pay for taxis, groceries, subscriptions, flights and bookings through Airbnb or Booking. At the same time, your old bank card may no longer work abroad, while a local bank may not be ready to open an account for you right away.

For expats, relocators, digital nomads and people moving abroad long term, this can become one of the most stressful parts of the move. You may have money, but using it is not always easy. Some services accept only local cards. Some landlords request a bank transfer. Some platforms require an IBAN, proof of address, residence permit, tax number or local phone number.

A virtual card for expats helps you avoid depending on a local bank, both during the first weeks after relocation and later. It can be used as a full payment tool for online payments, bookings, subscriptions, travel expenses, digital services and everyday purchases.

This is especially useful when the card is issued without KYC, can be topped up with crypto and supports Apple Pay or Google Pay. For a relocator, this is not just a temporary solution before opening a local bank account. It is a way to keep financial flexibility in any country.

Why the First Months Abroad Are a Financial Risk Zone

Relocation rarely goes exactly as planned. Even if you have savings, tickets, temporary housing and a clear route, you may arrive in a new country and find out that your usual payment tools no longer work the way they used to.

The first problems usually appear around basic everyday expenses, not big purchases. You need to pay for housing, buy a SIM card, call a taxi, connect internet, buy groceries, get insurance, pay for work tools, renew subscriptions and add a card to local apps.

At this stage, a card for relocators becomes more than a convenience. It becomes a way to keep daily life under control.

How Long It Really Takes to Open a Local Bank Account

Opening a local bank account can take from a few days to several weeks. In some countries, the process is fast if you already have a residence permit, rental agreement, tax number, local phone number and proof of address. In other cases, the bank may ask for extra documents, proof of income, source of funds or an in person visit to a branch.

The problem is often not the bank itself, but the document chain. To open an account, you may need an address. To get an address, you need to rent an apartment. To rent an apartment, you need to pay a deposit. To pay a deposit, you need a card or a bank transfer.

This creates a loop where every next step depends on the previous one. That is why a card without a local bank can make life much easier after relocation.

What Is Hard to Do Without a Working Card

Without a working card abroad, even simple tasks can become complicated. The biggest limitations usually appear in online services and everyday payments.

Without a card, it may be difficult to:

- Book accommodation through Airbnb or Booking.

- Pay for a hotel during the first days.

- Buy a flight or train ticket.

- Connect mobile service or eSIM.

- Pay for insurance.

- Activate work related subscriptions.

- Pay for taxis and delivery apps.

- Add a payment method to local services.

- Pay a rental deposit through an online platform.

- Buy equipment or work tools.

For freelancers, digital nomads, remote employees and entrepreneurs, this is especially important. If the card does not work, it affects not only daily life, but also work.

Why Payment Conditions Differ From Country to Country

Financial rules for non residents vary widely depending on the country, bank and document requirements. In one country, you may be able to open a basic account quickly. In another, you may need proof of residence, a tax number, a long term rental agreement or official status.

Payment requirements also differ. Some services accept international cards with no issues. Others work only with local cards. Some government portals, mobile operators, landlords or insurance companies may accept only a local bank transfer.

That is why a virtual card for long term travelers or expats helps you stay less dependent on local banking infrastructure and continue paying in a familiar way.

What Options Do Expats Have

Expats usually have several options: use an international fintech service, open a local bank account, get a virtual card from an international issuer or combine several tools.

The best option depends on the country, documents, income currency, source of funds, payment urgency and how quickly you need to start using a card.

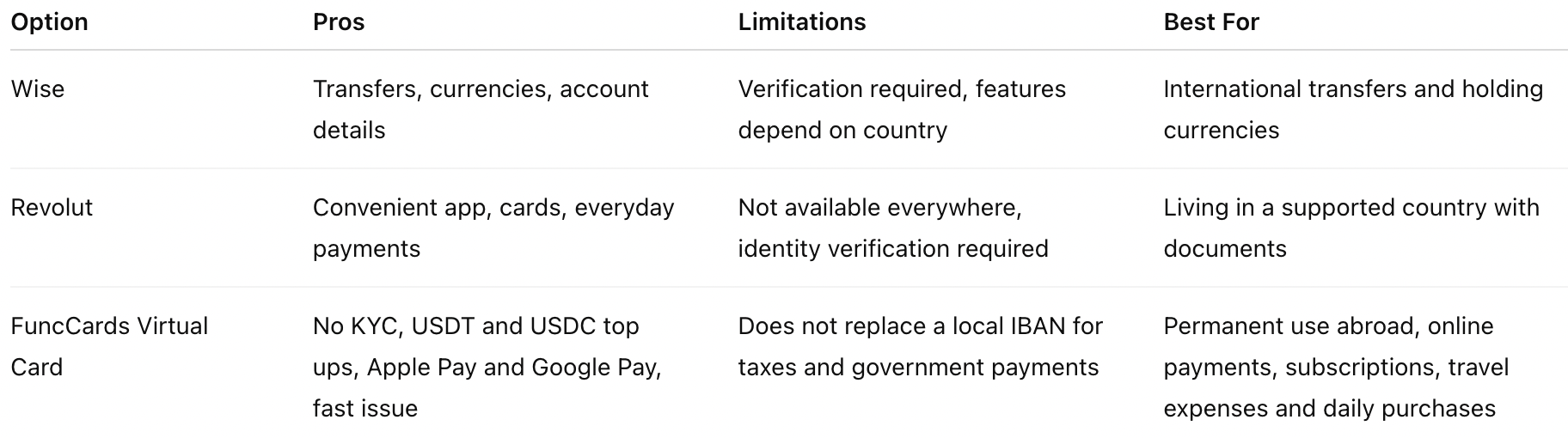

Wise: Pros and Limitations

Wise is often used for international transfers, holding money in different currencies and receiving account details in selected regions. It is useful for people who need to send money between countries, convert currencies and pay abroad.

Pros of Wise:

- Convenient currency conversion.

- International transfers.

- Ability to hold balances in different currencies.

- Transparent fee structure.

- Useful for freelancers and remote specialists.

Limitations:

- Available features depend on the country of residence.

- Identity verification may be required.

- Proof of address may be required.

- Not all currencies and account details are available to all users.

- Card availability depends on the region.

Wise can be a good tool for transfers and currency management, but it does not always solve the problem for someone who has just arrived and cannot yet confirm address or residence status.

Revolut: Pros and Limitations

Revolut is convenient for everyday payments, travel, currency exchange and managing money in an app. For many expats, it can be a strong option if the service is available in their country of residence and they can pass verification.

Pros of Revolut:

- Convenient mobile app.

- Virtual and physical cards.

- Currency operations.

- Contactless payments in supported countries.

- Useful for travel expenses and daily purchases.

Limitations:

- Account opening is not available everywhere.

- Identity verification is required.

- A local address may be required.

- Some features depend on the region.

- It may not be the fastest option for people who have just moved and cannot yet confirm residence.

Revolut can be useful once you already have a clear status, address and access to the service in your new country. But during the first days after relocation, it is not always the fastest payment solution.

FuncCards Virtual Card: What It Gives You

A FuncCards virtual card covers much more than the first basic payments after relocation. For expats, digital nomads, freelancers and long term travelers, it can become a full alternative to a bank card for everyday payments.

The main advantage is independence from a local bank. You do not need to wait for a residence permit, collect a full document package, confirm your address or go through a long bank review to start paying abroad.

A virtual card is especially convenient because it:

- Is issued without KYC.

- Can be topped up with USDT and USDC.

- Is suitable for regular use abroad.

- Supports Apple Pay and Google Pay.

- Works for online purchases and subscriptions.

- Works for travel expenses, hotels, flights and bookings.

- Helps you avoid dependence on a local bank account.

For everyday expenses, you can use a multi currency debit card. If you need to start paying quickly without complex verification, a prepaid card without verification can be a better fit.

Comparison of Options

How to Open a Virtual Card Without a Residence Permit or Local Bank

The main challenge after relocation is simple: you need to pay immediately, but you may not yet have the documents required by a local bank. Not everyone has a residence permit, local tax number, proof of address, rental agreement or local phone number.

That is why a no KYC card is a practical solution for people who want quick access to payments without long banking bureaucracy.

With FuncCards, you do not need to go through a complex bank review or wait for an account in your new country. The card is issued online, can be topped up with crypto and can be used for regular payments abroad.

This format is especially useful for:

- Expats.

- Digital nomads.

- Freelancers.

- Long term travelers.

- Remote teams.

- People who receive income in crypto.

- Anyone who does not want to depend on a local bank.

If you want to understand the topic of cards without identity checks in more detail, you can also read this guide: how to open an anonymous card.

What You Need to Issue a Card

Unlike a traditional local bank, a virtual card does not require a long process with a branch visit, proof of address and waiting for approval.

In a basic scenario, the user needs to:

- Register in the service.

- Top up the balance with crypto.

- Issue a virtual card.

- Add it to Apple Pay or Google Pay for contactless payments.

- Use the card for online and offline payments.

This format is especially useful when you need to start paying quickly: for housing, flights, insurance, services, mobile connection or work tools.

How Long Card Issuing Takes

A virtual card is usually issued much faster than a local bank card. Once the account is created and the balance is topped up, issuing a card can take only a few minutes.

This is useful when you need to pay for a booking, renew a subscription, buy a ticket or confirm a payment method in a service.

What Limits You Should Check

Even if the card is issued quickly, it is important to check the terms and limits before using it. This matters especially if you plan to pay for rent, a deposit, flights or larger purchases.

Before making a payment, check:

- Maximum balance.

- Limit per transaction.

- Daily limit.

- Monthly limit.

- Top up fee.

- Currency conversion fee.

- Apple Pay and Google Pay support.

- Supported merchants and countries.

If the payment amount is high, it is better to check in advance that the card limit is suitable for that transaction.

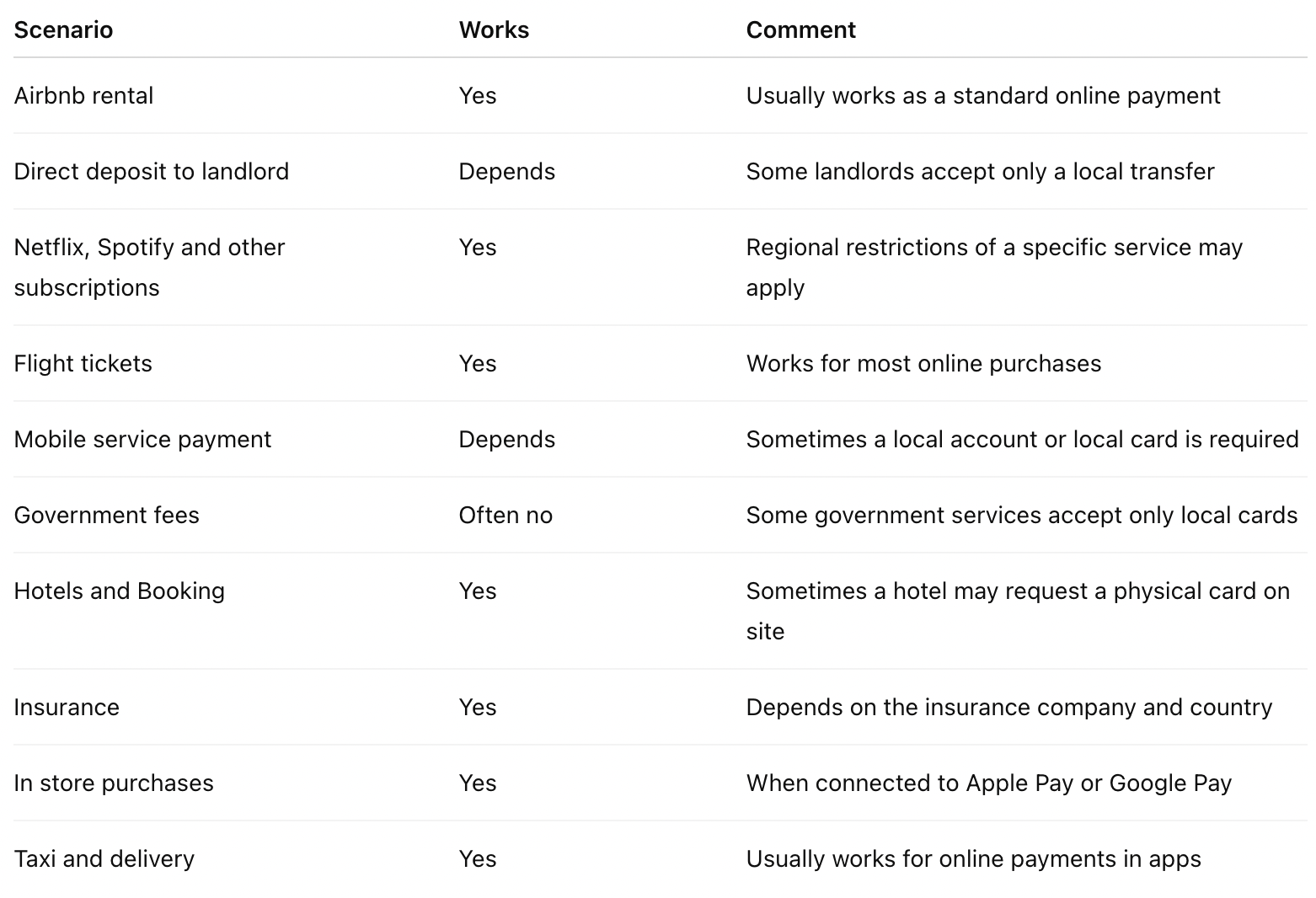

What You Can and Cannot Pay for With a Virtual Card

A virtual card helps cover most everyday, work and travel payments abroad. You can use it online, for subscriptions, bookings, tickets, services and everyday purchases through Apple Pay or Google Pay.

However, some situations may still require a local bank account. For example, certain government services, local operators or landlords may accept only local cards or bank transfers.

If you plan to use the card not only online, but also in stores, cafes, transport and trips, set up contactless payment through Apple Pay in advance.

How to Top Up a Virtual Card While Living Abroad

A card for relocation is useful only if it is easy to top up. One of the main advantages of FuncCards is that the card can be topped up with crypto.

This is especially important abroad when you do not have a local bank account, bank transfers are inconvenient or you do not want to connect all payments to the local financial system.

FuncCards supports USDT and USDC top ups, so the card can be used as a permanent payment tool for living, working and traveling abroad.

From a USDT and USDC Crypto Wallet

Top ups with USDT and USDC are convenient if you receive income in crypto, work with international clients, freelance or simply want a payment tool that is not tied to one specific country.

Advantages of this approach:

- No local bank is needed.

- No need to wait for account opening.

- You can top up the balance from any country.

- Convenient if your income comes in USDT or USDC.

- Suitable for regular expenses, subscriptions, bookings and travel payments.

- The card can be used permanently, not only during the first months after relocation.

- The card can be added to Apple Pay and Google Pay, so it is convenient for both online and offline payments.

Before topping up, check the transfer network, fees and service rules.

From a Foreign Account

If you already have an account in another country, you can use it as an additional source of funds. This is useful if you opened an international account in advance, receive payouts to a foreign account or use fintech services.

For many expats, this option is not available immediately. That is why crypto top ups are often a more flexible way to use a card without a local bank.

From an Employer or Client

Freelancers, consultants, developers, designers, media buyers and other remote specialists often receive payments from clients in different countries. For them, it is important not only to receive money, but also to quickly turn it into a usable payment tool.

If you work on projects or through gig platforms, you can consider a solution for freelancers to separate personal, work and travel expenses.

Security Abroad

When you are in another country, losing access to money feels much more serious. That is why a virtual card should be not only convenient, but also safe.

What to Do If You Lose Access While Abroad

If you lose access to your card, phone or account, act quickly.

Basic steps:

- Block the card in the app or through support.

- Check recent transactions.

- Change your account password.

- Check access to your email.

- Restore two factor authentication.

- Issue a new card if the service allows it.

- Do not keep your entire budget on one card.

It is better to have a backup payment method in advance. For example, a second virtual card, cash for a few days and separate access to your main account.

Two Factor Authentication Without a Local Phone Number

One common issue for expats is that the old SIM card stops working, while the local number has not been set up yet. If two factor authentication is connected only to the old number, you may lose access to financial services.

Before moving, it is worth doing the following:

- Update the phone number in important services.

- Add email as a backup channel.

- Set up an authentication app.

- Save backup codes.

- Check email access from a new device.

- Do not use one phone number for all services.

It is also important to choose services with fraud protection, transaction monitoring and the ability to quickly block a card.

Financial Checklist for the First Month After Moving Abroad

- Check whether your current cards work in the new country.

- Issue a virtual card before moving or during the first days after arrival.

- Top up the card with USDT or USDC to get quick access to payments.

- Add the card to Apple Pay or Google Pay for offline payments.

- Keep money in at least two different places.

- Check top up and currency conversion fees in advance.

- Prepare backup access to email and two factor authentication.

- Save support contacts for your payment service.

- Check limits for rent, flights, insurance and larger purchases.

- Start collecting documents for a local bank if you need it for taxes, government services or long term rent.

When You Need a Local Bank and When a Virtual Card Is Enough

A virtual card can be a full alternative to a bank card for most everyday payments abroad. You can use it to pay for online purchases, subscriptions, flights, hotels, services, travel expenses, food, transport and in store purchases through Apple Pay or Google Pay.

A local bank may be needed only for tasks where a local account or IBAN is required:

- Receiving salary from a local employer.

- Paying taxes.

- Government fees and public services.

- Long term rent if the landlord accepts only a bank transfer.

- Local services that work only with cards issued by local banks.

- Building banking history in the new country.

If you do not need these tasks, a virtual card may be enough for permanent use. This is especially true if you work remotely, often change countries, receive income in crypto or do not want to depend on the local banking system.

For many expats, the best setup is not one single tool, but a combination: a virtual card for regular payments, a local bank for official tasks and a backup way to access funds.

FAQ

Can I Get a Card Without a Residence Permit?

Yes. You can get a FuncCards virtual card without a residence permit and without a complex bank review. This is convenient for expats, digital nomads and people who have just moved or often change countries.

Is KYC Required to Issue a Card?

No. FuncCards issues cards without KYC. This is one of the key advantages for people who do not want to go through a long verification process, upload documents and wait for local bank approval.

Can I Use the Card to Pay Rent?

For rent through Airbnb, Booking or similar platforms, a virtual card usually works. If you pay a landlord directly, it depends on the landlord’s requirements. Some accept card payments, while others require a bank transfer to a local account.

Can I Receive Salary on This Card?

A virtual card is mainly designed for payments, purchases, subscriptions and travel expenses. If an employer requires an IBAN or a local bank account, you may need a bank or a fintech service with account details. But if you receive income in crypto or from international clients, you can top up the card with USDT and USDC and use it for regular expenses.

What Should I Do If the Card Is Blocked Abroad?

Block the card, check transactions, contact support and issue a new card if the service allows it. During recovery, use a backup card or another payment method. This is why it is better not to keep your entire budget on one card.

Is Apple Pay Supported in a New Country?

If the card supports Apple Pay, you can add it to Wallet and use it for contactless payments wherever Apple Pay is accepted. FuncCards also supports Google Pay, which makes the card convenient for both online and offline payments.

What Is the Currency Conversion Fee?

The fee depends on the card currency, payment currency and service terms. If you live in a country with a different currency, check the rate, conversion fee and possible additional charges in advance.

Are There Country Restrictions?

Restrictions may exist for specific merchants, services or government websites. Some local services accept only cards issued by local banks. Before making a large payment, check whether the card is suitable for that specific transaction.

Read Also

- How to Open an Anonymous Virtual Card Without Verification and a Passport

- How to Spend USDT in Everyday Life

Conclusion

Moving abroad often creates a financial gap: you need to pay right away, while a local bank may be unavailable because of documents, residence status, address or long review times. But that does not mean you need to wait for a local account to use your money normally.

A FuncCards virtual card is not only useful during the first weeks after relocation. It is a full payment tool for permanent use abroad. The card is issued without KYC, can be topped up with USDT and USDC, supports Apple Pay and Google Pay and works for online payments, subscriptions, bookings, travel expenses and everyday purchases.

For expats, digital nomads, freelancers and long term travelers, it is a way to pay in different countries without being tied to a local bank or unnecessary bureaucracy.

Register with FuncCards and issue a virtual card for life, work and payments abroad.